Overview

The school will focus on how to use machine learning to adress the gap that exists between conventional models in financial mathematics and the understanding of a model of the world that often lacks practical applicability, enabling more accurate modeling of financial markets and informed decision-making.

It will consist of five introductory courses and many other talks. The presentations, given by young scientists, will provide further insight into the various research branches of the field of this school.

Organizing Committee

Scientific Committee

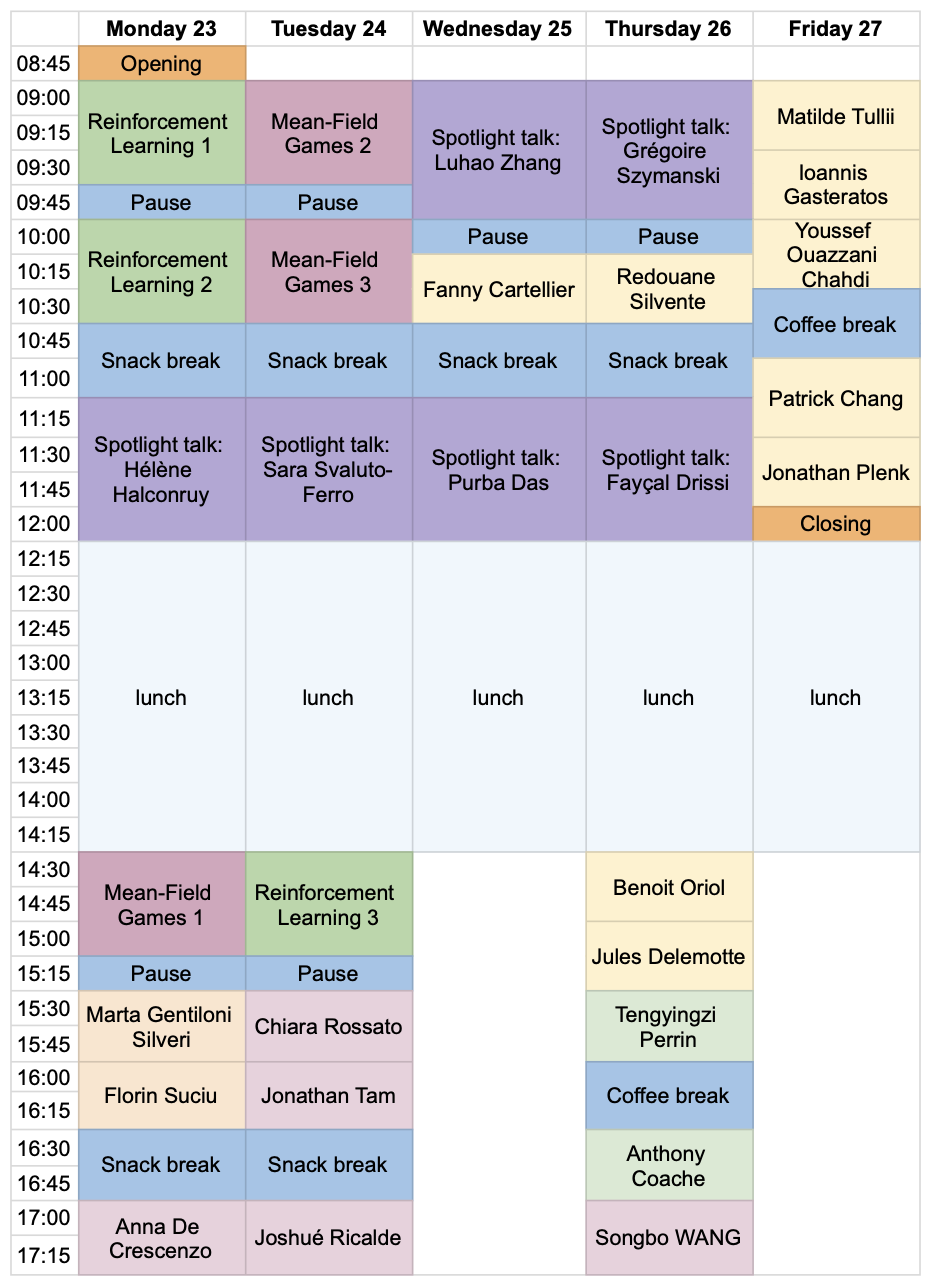

Program

In order to foster collaboration and discussion, we will host three types of talks broken up by many short breaks, namely:

- 5 Introductory courses (one for each thematic session) each consisting of 3 lectures of 45 minutes each.

- 7 Spotlight talks dedicated to exemplary interdisciplinary work or industry relevant problems lasting 45 minutes each (35m talk, 10m questions).

- 20 Short talks with posters encouraged, lasting 20 minutes each (15m talk, 5m questions).

The workshop focuses on interdisciplinary contributions at the intersection of Applied and Financial Mathematics, Statistics, Economics, and Computer Science, welcoming both theoretical and empirical work. The objective is to build bridges between these communities at the level of young researchers to forge connections that will drive interdisciplinary research forward in the future.

Venue

The workshop will take place at the Centre Paul Langevin, in Aussois, in the French Alps.

It is accessible by trains up to Modane Station on the French side or Bardonecchia on the Italian side, then by taxi.